Pago Pago, AMERICAN SAMOA — The American Samoa Visitors Bureau “needs improved controls over its purchasing and payment processes” is one of the findings identified by the Territorial Audit Office during its Performance Audit of the Bureau for fiscal years ending Sept. 30, 2022.

Part two of the Samoa News coverage of the TAO audit looks at this finding, where the auditors point out that the Bureau’s total expenditures showed a reduction of 18.8 percent from 2020 to 2021 and an increase of 22.8 percent from 2021 to 2022. And with approximately $400,000 to $500,000 spent annually for goods and services.

The performance audit report — to the governor as well as the Fono, which was released last week — noted that the Bureau has various rules, policies and procedures with which it must comply when procuring supplies and services.

It explains that depending on the need of the Bureau and the dollar amount of the goods or services, the Bureau applied different methods such as Purchase Orders, Bidding, and Non-Purchase Order payments. The Bureau has various controls in place to ensure that payments are valid, accurate, and permitted.

Additionally, the Bureau employs an outside bookkeeping service contracted to process its payments. Specifically, TAO found the following issues in the procurement and payment processes:

• The Bureau accepted vendor services without executing written contracts, which demonstrates inconsistencies with procurement and purchasing requirements.

• The Bureau did not issue Purchase Orders for all purchases requiring a Purchase Order

• The Bureau did not secure required supporting documentations for payments in vendor files.

“The Bureau accepted vendor services without execution of written contracts, which demonstrates inconsistencies with procurement and purchasing requirements,” the auditors said and cited provisions of local law, pertaining to “Powers and duties of the Bureau” that allows the Bureau to make contracts, as authorized in this chapter.

“During our review, we found that contracts were not properly executed,” said TAO, and points out that its “audit established that the administration and oversight process, which requires completed agreements and or arrangements to ensure compliance with provisions of the law, was not sufficient. Improperly executed contracts are not valid under the law and may be unenforceable and put the Bureau at risk of liability.”

Furthermore, the “processing of payments without executed contracts should not be approved. Moreover, we considered that the sample selected in our testing are questionable costs.”

Data in the report shows a summary of charges paid to vendors without properly executed contracts. For bookkeeping services — $20,643 in FY 2020; $15,820 in FY 2021; and $23,211 in FY 2022. “Other professional services” shows $30,746 in FY 2020; $9,500 in FY 2021; and $10,681 in FY 2022. There’s also a payment of $10,000 in FY 2022 for “other contract services.”

PURCHASE ORDERS

“Purchase Orders were not issued for all purchases,” said TAO, which explained that Purchase Orders allow the Bureau to purchase goods and services from different vendors and then authorizes the payment to the vendor or service provider.

The Purchase Order justifies the request and justification for purchase(s). The procurement of goods and services are governed by the Bureau’s Purchasing and Receiving Internal Control Policy manual with the following key procedures.

However, TAO said that: “Our sample of payments found that 10 purchases requiring Purchase Orders were processed without purchase orders. These purchases totaled $36,382.06”.

SUPPORTING DOCUMENTS

“The Bureau did not secure required supporting documentations for payments in its vendor files,” according to the auditors who noted that the procurement of goods and services are governed by the Bureau’s Purchasing and Receiving Internal Control Policy manual.

TAO’s sample of 65 payments revealed that: nine purchases totaling to $62,450 lacked vendor invoices; and eight purchases totaling to $28,889.13 lacked receiving reports issued, according to the report.

“We could not confirm whether vendor invoices were obtained at the time of payment processing or whether receiving reports were issued when the supplies and services were delivered,” the auditors said.

RECOMMENDATIONS

TAO offered three recommendations, and one of them is that the Board of directors should appropriately review and amend where necessary provisions of the Code, policies, and procedures to ensure compliance.

“If the Bureau is unable to adequately address its deficiencies, the Board should consider adopting best practices or techniques to help and avoid problems in the administration of contracts,” TAO said.

“Best practices are practical techniques gained from practical experience that may be used to improve the process,” the auditors said and the Bureau acknowledged this recommendation.

The second TAO recommendation is that the Bureau must comply with its written procurement procedures without exception. Additionally, the Bureau’s finance personnel should ensure purchase orders are issued for all purchases. In response, the Bureau said it will move forward with improvement.

TAO’s third recommendation: the Bureau must comply with its written procurement procedures without exception. The Bureau’s finance personnel should ensure receiving reports are issued for all supplies received; Receiving Reports are prepared to confirm validity of purchases received.

And the Bureau, in its response, acknowledged this recommendation.

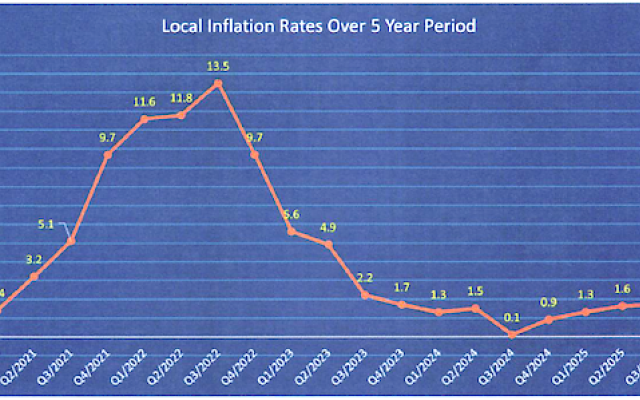

is -1.3% this quarter. Among the thirty food items that have seen a price drop, one item significantly contributed to this decline, eggs.")

Comments

Sorted by BestComments are powered by Disqus. By commenting, you agree to their privacy policy.

Powered by Disqus