Pago Pago, AMERICAN SAMOA — The American Samoa Visitors Bureau “needs better controls over its fixed assets” is another finding identified by the Territorial Audit Office during its Performance Audit of the Bureau for three fiscal years ending Sept. 30, 2022.

Part five of the Samoa News coverage of the TAO audit looks at this finding, with the auditors saying that the Bureau categorizes fixed assets as capital items acquired with a purchase price of $1,000 or more and with a useful life of more than one year. And the Executive Director approves purchases up to $5,000 and the Board of Directors approves purchases over $5,000.

TAO noted that the Bureau has established policies and procedures specifying — among other things — fixed assets shall be recorded when acquired and the Bureau is responsible for all assets, tagged and assigned, and maintained in a fixed asset listing.

Although a fixed asset listing is maintained, TAO auditors said, the accuracy and completeness cannot be determined.

“This increases the risk of unrecorded assets, overstated or understated asset values, and unknown asset conditions only to name a few,” said TAO, which noted that the Bureau didn’t conduct an inventory of all its fixed assets; follow its procedures for disposing of fixed assets; follow its capitalization policy; and establish sufficient controls for fixed assets.

Among the concerns raised by the auditors is that the Bureau did not carry out a department-wide annual physical count. TAO performed physical inventory, which revealed that fixed assets were not inventoried. Following the asset verification, it is likely that the value in the financial records and number of assets has reduced.

“However, the asset verification process did not address the specific risk of fully depreciated assets. A physical inventory is essential to ensure the accuracy of fixed assets as reported in the financial reports,” said TAO.

In addition, if fixed assets are not adequately tracked and inventoried, losses or misappropriations may go undetected, according to the auditors, who provided a summary of specific list of assets it surveyed and that several assets could not be located and others were disposed.

TAO went on to point out that the Bureau did not follow proper procedures when disposing of fixed assets. “We found that the Bureau did not go through the disposition procedures in that disposition forms shall be filled out as required,” the auditor said.

And the asset verification revealed that four fixed assets were disposed but could not verify that disposition forms were properly filled out and approved.

Another concern on fixed assets raised by the auditors is that “Bureau did not follow its capitalization policy”. TAO noted that Internal Control Policy on Fixed Asset Control states, any internally constructed donated equipment is recorded by the Executive Assistant if the item cost has a value of $1,000 or more.

A complete description of the property, date constructed or received, number of items, cost of estimated value and a statement that it was internally constructed or donated will be included in the report.

The capitalization threshold policy is the minimum purchase amount that would require recording as an asset and capitalizing rather than expensing as a period cost.

“Our disbursement testing revealed that a payment of $2,627.40 for the purchases of tents was expensed rather than capitalizing the asset. We could not locate this item during our spot verification,” the auditors said.

In conclusion, TAO found that the “Bureau lacks sufficient controls” of its fix assets. “As a result, losses of fixed assets could go undetected,” said TAO, which identified the following “problems”:

• Fixed assets records were not reconciled — the audit verification could not be reconciled with financial records

• Some fixed assets could not be located — our asset verification identified 12 assets were not found

Among the four TAO recommendations, cited in the report, is for the Bureau to perform a complete physical count of all its fixed assets as soon as possible — which the Bureau responded that “actions being taken to mitigate findings.” Additionally, the Bureau’s policies and procedures should not be circumvented when disposing of fixed assets.

Furthermore, the Bureau should conform to its capitalization threshold policy that all capital items purchase of $1,000 and more and with a useful life of more than one year should be recorded as a fixed asset.

The 4th recommendation is that the Bureau should ensure that it complies with the following requirements:

• Reconcile the physical inventory to the inventory records

• Investigate and resolve all inventory variances

• Correct inventory records in QuickBooks to reflect the current on-hand balances/quantities and ensure records are accurate and properly maintained.

In it’s response, acknowledging the four recommendations, the Bureau explained that the listed fixed assets in the audit report were purchased between 2009-2018 and it will update records.

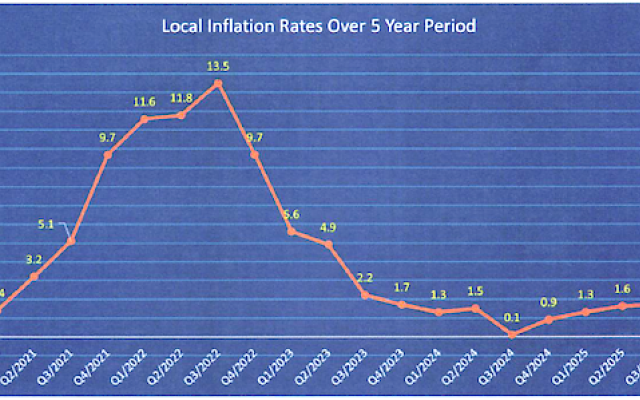

is -1.3% this quarter. Among the thirty food items that have seen a price drop, one item significantly contributed to this decline, eggs.")

Comments

Sorted by BestComments are powered by Disqus. By commenting, you agree to their privacy policy.

Powered by Disqus